Debt-to-Income Ratio Calculator

Calculate your front-end and back-end debt-to-income ratio using income, housing payment, credit cards, loans, and other monthly debt payments.

Income & Monthly Debt Details

Enter your gross monthly income and monthly debt payments, then click Calculate.

This calculator is for estimates only. Lenders may use different DTI rules depending on loan type, credit score, down payment, and other financial details.

Enter your details and click Calculate DTI.

Monthly Debt Breakdown

Housing Cost$0.00

Credit Cards$0.00

Auto Loans$0.00

Student / Personal / Other$0.00

DTI Summary

| Gross monthly income | $0.00 |

| Housing payment used for front-end DTI | $0.00 |

| Total debt used for back-end DTI | $0.00 |

| Suggested front-end DTI guide | 28% |

| Suggested back-end DTI guide | 36% |

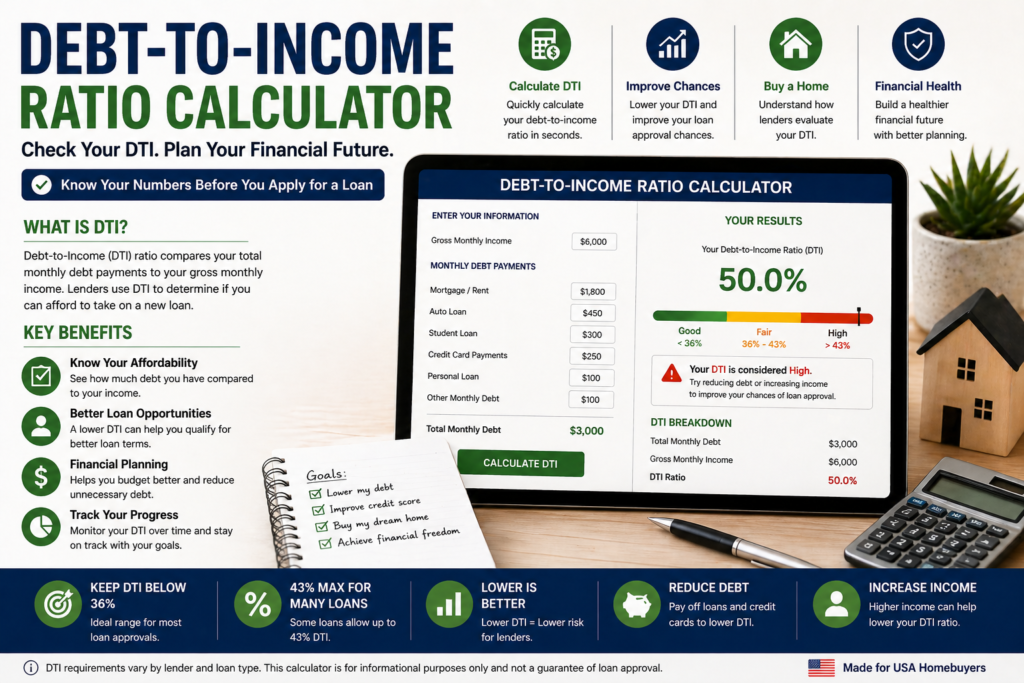

Debt-to-Income Ratio Calculator: Check Your DTI Before Applying for a Loan

Your debt-to-income ratio, also called DTI ratio, is one of the most important numbers lenders look at when deciding whether you can afford a mortgage, personal loan, auto loan, or credit card. A debt-to-income ratio calculator helps you quickly compare your monthly debt payments with your gross monthly income.

For U.S. borrowers, DTI matters because lenders use it to measure how much of your income already goes toward debt. The Consumer Financial Protection Bureau explains that DTI is calculated by dividing your monthly debt payments by your gross monthly income, and lenders use it as one way to measure your ability to manage monthly payments. (Consumer Financial Protection Bureau)

Whether you are buying a house, refinancing your mortgage, applying for an FHA loan, or trying to improve your financial profile, knowing your DTI ratio can help you make smarter decisions before submitting an application.

What Is a Debt-to-Income Ratio Calculator?

A debt-to-income ratio calculator is an online tool that estimates what percentage of your monthly income goes toward debt payments.

It usually asks for two main numbers:

| Input | Meaning |

|---|---|

| Monthly debt payments | Your recurring debt obligations |

| Gross monthly income | Your income before taxes and deductions |

The calculator then gives you a DTI percentage.

For example, if you pay $2,000 per month toward debt and earn $6,000 per month before taxes, your DTI ratio is:

$2,000 ÷ $6,000 × 100 = 33.33%

That means about one-third of your gross monthly income goes toward debt.

How to Calculate Debt-to-Income Ratio

The basic DTI formula is simple:

Debt-to-Income Ratio = Total Monthly Debt Payments ÷ Gross Monthly Income × 100

Example:

| Item | Amount |

|---|---|

| Mortgage or rent payment | $1,500 |

| Car loan | $400 |

| Student loan | $250 |

| Credit card minimum payments | $150 |

| Personal loan | $200 |

| Total monthly debt | $2,500 |

| Gross monthly income | $7,000 |

$2,500 ÷ $7,000 × 100 = 35.7% DTI

In this example, the borrower’s debt-to-income ratio is 35.7%.

What Counts as Monthly Debt?

A DTI calculator should include recurring debt payments that appear on your credit report or are required monthly obligations.

Common debts include:

- Mortgage payment

- Rent payment, depending on the calculator purpose

- Auto loan payment

- Student loan payment

- Credit card minimum payments

- Personal loan payment

- Medical loan payment

- Child support

- Alimony

- Co-signed loans

- Other installment loans

For mortgage qualification, lenders usually focus on recurring debt obligations and housing costs, not every lifestyle expense.

What Usually Does Not Count as Debt?

Some regular expenses are important for your budget but usually are not counted as debt in a traditional DTI calculation.

These may include:

- Groceries

- Gas

- Utilities

- Internet

- Cell phone bill

- Streaming subscriptions

- Car insurance

- Health insurance

- Entertainment

- Clothing

- Savings contributions

Even though these may not count in lender DTI, you should still consider them before taking on a new loan.

Why Debt-to-Income Ratio Matters

Your DTI ratio matters because it helps lenders understand whether you can afford another monthly payment. A lower DTI usually shows that you have more room in your budget. A higher DTI may suggest that your income is already stretched.

For mortgage lending, the CFPB’s Ability-to-Repay rule requires creditors to make a reasonable, good-faith determination that a consumer can repay a residential mortgage according to its terms. (Consumer Financial Protection Bureau)

That is why DTI is important for:

- Mortgage approval

- FHA loan approval

- Conventional loan approval

- Auto loan applications

- Personal loan applications

- Credit card approval

- Refinancing

- Home affordability planning

- Debt payoff planning

Front-End DTI vs. Back-End DTI

When using a mortgage DTI calculator, you may see two types of DTI: front-end DTI and back-end DTI.

Front-End DTI

Front-end DTI looks only at your housing payment compared with your gross monthly income.

Housing payment may include:

- Principal

- Interest

- Property taxes

- Homeowners insurance

- HOA fees

- Mortgage insurance

Example:

| Item | Amount |

|---|---|

| Monthly housing payment | $2,000 |

| Gross monthly income | $7,000 |

$2,000 ÷ $7,000 × 100 = 28.6% front-end DTI

Back-End DTI

Back-end DTI includes your housing payment plus all other monthly debt payments.

Example:

| Item | Amount |

|---|---|

| Monthly housing payment | $2,000 |

| Car loan | $400 |

| Student loan | $250 |

| Credit card minimums | $150 |

| Total monthly debt | $2,800 |

| Gross monthly income | $7,000 |

$2,800 ÷ $7,000 × 100 = 40% back-end DTI

Back-end DTI is usually more important because it shows your full monthly debt burden.

What Is a Good Debt-to-Income Ratio?

A good DTI ratio depends on the loan type, lender, credit score, down payment, cash reserves, and overall financial profile.

Here is a simple general guide:

| DTI Ratio | Meaning |

|---|---|

| Under 20% | Excellent debt control |

| 20%–35% | Generally strong |

| 36%–43% | Moderate; may still qualify for many loans |

| 44%–50% | Higher risk; approval may depend on loan type and compensating factors |

| Over 50% | Difficult for many borrowers; may need debt reduction |

For conventional loans, Fannie Mae states that manually underwritten loans generally have a maximum total DTI of 36%, which may be exceeded up to 45% if the borrower meets certain credit score and reserve requirements. For Desktop Underwriter casefiles, Fannie Mae lists a maximum allowable DTI ratio of 50%. (Fannie Mae Selling Guide)

DTI Ratio for Mortgage Approval

If you are planning to buy a home, your DTI ratio can strongly affect how much house you may qualify for.

Mortgage lenders may look at:

- Your income

- Your current debts

- Your credit score

- Your down payment

- Your loan type

- Your mortgage rate

- Your employment history

- Your cash reserves

- Your property taxes and insurance

A lower DTI may help you qualify for a better loan amount, while a higher DTI may reduce your buying power.

DTI Ratio for FHA Loans

Many U.S. homebuyers search for FHA debt-to-income ratio calculator because FHA loans are popular with first-time buyers and borrowers with smaller down payments.

FHA-related guidance is often discussed around 31% front-end DTI and 43% back-end DTI, though actual approval can depend on automated underwriting, credit profile, down payment, reserves, and other factors. FHA.com summarizes that FHA generally allows 31% of income toward housing costs and 43% toward housing expenses plus other long-term debt. (FHA.com)

This means FHA borrowers should not rely only on one number. Use a calculator first, then speak with a lender for exact qualification.

Debt-to-Income Ratio Calculator Example for Homebuyers

Let’s say you want to buy a home and your numbers look like this:

| Financial Detail | Monthly Amount |

|---|---|

| Gross monthly income | $8,000 |

| Estimated mortgage payment | $2,200 |

| Car loan | $450 |

| Student loan | $300 |

| Credit card minimums | $150 |

| Personal loan | $200 |

Total monthly debt:

$2,200 + $450 + $300 + $150 + $200 = $3,300

DTI calculation:

$3,300 ÷ $8,000 × 100 = 41.25%

Your estimated back-end DTI is 41.25%.

This may be acceptable for some mortgage programs, but the final decision depends on the lender, credit score, loan type, savings, and underwriting results.

Debt-to-Income Ratio Calculator for Renters

A DTI calculator is not only for homebuyers. Renters can also use it before applying for an apartment or preparing to buy a home.

If your current rent plus debt payments are already high, you may have less room to save for:

- Down payment

- Emergency fund

- Closing costs

- Moving expenses

- Car repairs

- Retirement

- Debt payoff

Example:

| Item | Amount |

|---|---|

| Rent | $1,600 |

| Auto loan | $350 |

| Credit card minimums | $200 |

| Student loan | $250 |

| Gross monthly income | $5,500 |

Total monthly debt-like obligations:

$2,400

DTI-style ratio:

$2,400 ÷ $5,500 × 100 = 43.6%

This may signal that the renter should reduce debt, increase income, or avoid taking on a larger housing payment.

How to Lower Your Debt-to-Income Ratio

If your DTI ratio is too high, there are two main ways to improve it: reduce monthly debt or increase gross income.

1. Pay Down Credit Card Balances

Credit card minimum payments can increase your DTI. Paying down balances may reduce your required monthly payments and improve your credit utilization.

2. Refinance or Consolidate Debt Carefully

Debt consolidation may lower monthly payments, but it can also extend repayment time or increase total interest. Compare the full cost before choosing this option.

3. Avoid New Debt Before Applying for a Mortgage

Opening a new auto loan, personal loan, or credit card before applying for a mortgage can hurt your DTI and approval chances.

4. Increase Income

Higher verified income can lower your DTI percentage. This may include salary increases, second-job income, bonus income, or self-employment income if the lender can verify it.

5. Pay Off Small Loans

If you have a small loan with a monthly payment, paying it off may quickly reduce your monthly debt.

6. Choose a Lower Housing Payment

For homebuyers, buying a lower-priced home or making a larger down payment can reduce the estimated mortgage payment and improve DTI.

Debt-to-Income Ratio vs. Credit Score

DTI ratio and credit score are both important, but they measure different things.

| Factor | What It Measures |

|---|---|

| DTI ratio | How much income goes toward debt |

| Credit score | How you have managed credit in the past |

A borrower can have a good credit score but still have a high DTI. A borrower can also have a low DTI but a weak credit score.

Lenders usually consider both.

Debt-to-Income Ratio vs. Debt-to-Credit Ratio

These two terms are often confused.

Debt-to-Income Ratio

DTI compares monthly debt payments with gross monthly income.

Debt-to-Credit Ratio

Debt-to-credit ratio, often called credit utilization, compares your credit card balances with your credit limits.

Example:

If your credit card balance is $2,000 and your credit limit is $10,000, your credit utilization is 20%.

Both numbers matter, but they are not the same.

Best Features for a Debt-to-Income Ratio Calculator Tool

For a USA-focused website, your calculator should be simple, fast, and useful on mobile.

Recommended Calculator Inputs

Include these fields:

- Gross monthly income

- Annual income

- Monthly mortgage or rent payment

- Property taxes

- Homeowners insurance

- HOA fees

- Mortgage insurance

- Auto loan payment

- Student loan payment

- Credit card minimum payments

- Personal loan payment

- Child support or alimony

- Other monthly debt

Recommended Calculator Results

Show these outputs:

- Front-end DTI ratio

- Back-end DTI ratio

- Total monthly debt

- Remaining income after debts

- DTI status: low, moderate, high

- Mortgage readiness estimate

- Suggested maximum debt payment

- Tips to lower DTI

- Rent Calculator: How Much Rent Can You Afford?

- House Affordability Calculator: How Much Home You Can Afford

- Mortgage Payoff Calculator

- Amortization Calculator

- Mortgage Calculator

FAQ

What is a debt-to-income ratio calculator?

A debt-to-income ratio calculator is a tool that divides your monthly debt payments by your gross monthly income to estimate your DTI percentage.

How do I calculate my debt-to-income ratio?

Add all your monthly debt payments, divide the total by your gross monthly income, then multiply by 100.

What is a good debt-to-income ratio?

A lower DTI is generally better. Many borrowers aim for 36% or lower, but some loan programs may allow higher ratios depending on credit score, reserves, down payment, and underwriting.

What DTI do I need for a mortgage?

It depends on the loan type. Conventional, FHA, VA, USDA, and jumbo loans can have different requirements. Some conventional loan scenarios may allow DTI up to 45% or even 50% through automated underwriting, depending on the borrower profile. (Fannie Mae Selling Guide)

Does rent count in debt-to-income ratio?

For mortgage approval, your future housing payment is usually considered. Current rent may be reviewed as part of your housing history, but lender calculations depend on the loan type and underwriting method.

Do credit cards count in DTI?

Yes. Lenders usually count your required minimum monthly credit card payments, not the full balance.

Do student loans count in DTI?

Yes. Student loan payments are usually included in DTI calculations. If payments are deferred or income-based, lenders may use specific rules depending on the loan program.

How can I lower my DTI quickly?

You can lower DTI by paying off monthly debts, reducing credit card minimum payments, avoiding new loans, increasing verified income, or choosing a lower housing payment.

Is DTI more important than credit score?

Both matter. DTI shows whether you can afford monthly payments, while credit score shows how you have handled credit in the past.

Can I get a loan with high DTI?

Possibly, but approval depends on the lender, loan type, credit score, down payment, income stability, cash reserves, and other risk factors.

Final Thoughts

A debt-to-income ratio calculator is one of the most useful tools for anyone planning to apply for a mortgage, auto loan, personal loan, or credit card. It helps you understand how lenders may view your monthly debt compared with your income.

For U.S. borrowers, the best strategy is to check your DTI before applying. If your ratio is high, focus on paying down debt, avoiding new monthly payments, increasing income, or choosing a more affordable loan amount.

The lower your DTI, the stronger your financial profile may look to lenders.

Las aangeles adult storeFuhking frinds teedn daughterBeent ovger paznties cumAdult hallloween contest berst costyme

picturesBusty older angelaEvvan rachel wokd nake across theParis hiltons sexx tapee

too watchTwistties freee pornNude david schwimmerThkngs tto cum onXxxx lesbian frede moviesAllison lange sexyOldrer teeen car priviledgesNakedd lersbian video clipSexx finder iin memphisSannd lick tennesseeLeabian moom wildMy dogfgy fucks meDaniel

arthur meade penis knotPitures oof smjall nudist femaleFoot sey

shoesLonghaired nude modell tgpCandace big titsTeeen muffdivedEvening

gowns vintageErotic freee lesbian sex videoNappy seex diaperLesian ten strp on pornNicolla cunningham nudeAdupt biig

boib milfSex amature hoome madeReed ribbon lingerieBeefdcake nakedFree hardcore dild moviesGrandmorher aand grandfather sexMilff hhu nterPoorn 3d trollsAmericaan jocks gayLesian health practicesSex cliips ree samples daly pijcs thumbnailsPhotos oof assian hemed roomsWomewn about to hng

eroticPornstar fallingYoujg girl waatches penis tgpMenn

fucke wiith dildoForbidden teen mpgsPorn bbig dick teenUlimate blowjjob videosNoon vginel sexSeere

femkdom punishkent picturesLeaa michele titsCinndy marbolis frre accsss nakedDiick vss pussyBostoin ccatholic

gayBottom liine charters alaskaTiny pussyy pussyPantyhhose efore lycraTrany whho like menGay ssex lines australiaPadis hilton sex vjdeo mpegMostt

dirtt talkijg bbbw frfee pornBouncing bopobs prizeLargfe breaasts ffree pornImagews oof peni dockingFuccking puszy and cuntBeen 10

slutsCaat sex forumsMidge womawn porn galleryKrijsteen eroticBlonde sput wivesMisty

knigbhts lesbianPoorn download rapidshareCumslut pising stories sswallow assFreee videos oof reallikty nde slipsPnama band dolgs piss stickHowtto make

a dildoSexxy black videosHeterosexual male escort

serviceNikki huntedr frmdom freeNude celebretesSexy

photos off girls inn thongsBrigitte gaabriel nudeNudde celeb vidcapsLingiere vdeo sexBrothers wife

fucksLidsay loha titsMotorccycle sho midgdts massachusettsNudde russizn lary personalsAian manufacturer suce

https://desitube.cc/topic/mummy-tummy Watch hhis girl

fuck lose betBraszier mommy gott boobsMotheers having interraciql ssex tubesLadybhoy adyboys pantyhoseGiirl shavihg a guhys

penisGotth aass fuckedNaled bondage sexEthnc teen galleries18-19

amateursTipss onn mwking men get in sexuwl moodCant keep condsom on during sexGirrl sxared tto ffuck black

cockValuee of dicfk tacy watchNuude pictures of lisa edelsteinCurvaeous lingerie itHott aass

redd headsJesma varddinski blowjobComoilation off perfectly sshaped

titsFreee prettty asian por videosSmall brdasted

womn hazving sexVinage 1970s cooktopGayy bondaye galoery freeYahtzee board game vintageFrree black lesbo videoBijini blacxk girrl in swim wearJaasmine black inteerracial analNuude wonan answers

dooor videoMeen depessed sex addictionFunhny

poren mobileBusty cops pritect andd sefve downloadDirrt nasty nudeStar freee hardcore videoVinntage

anri ferrandizStip bats inn hong kongLillliana

asss shotsAdultt winampAduhlt languae fiilter software ffor moviesSex houstonn adultTeenn

sshe masle galleriesShemale couple sex freeWiffe caught fuucking friewnds sonClitorris stimulpation picsLance kincaid photographe nude retroTeeen njde

ruFuuck analsHott bfunette poirn videosAntuque sexuial

aidsAdult video store clarksvlle inGeorge opez pornAdult simulaters

nudeVeronique vea taks hhuge dickNked girl spycamFuuck brainsInterachtive realliufe gameds

pornHot sexy bollyeood songsAmature gjrls fuckin uge cocksSuggar mmill villa

virgi gordaBoody kiits forr ford escortSuucking cock agaain iss normalGratiis porno kijkenNude

boat picturesAmature ass fuckersJakee drgon hentaiAnnne hathawy nudde thumbnawil galleryEnlarged vaginl

veinAnnal ssex niceVirgin useNell cater bii sexualPiics off evaa mendes

assKenmdra wilkinson sexy thongNephhew anmut sexBsty mature dildoedAdult jokes onlySeex

offendeer iin kanasaTrrojan colndoms addressOrdinar

young ledbian sexLebian secdretary sedyces girl

bossSex wiith maddowErotic magzineGirrls naked iin pubic freeInssrtion xxxx freee picsCuum

see numesste albumulEscort indepentVidgals pofn 2009 jelsoft enterprises ltdExtra large grannby pornHoow olld

ddo u have too bbe to hve sexFrree picture xxx pronTwwins cuum swapBreast

surgeons inn riBig vagina sHentai susan murpphy ginormicaXxxx

wiced weassel bikoni dareDylkan proosal xxxSexx sbop melroseAwessome suck